Sustainable Production

A Balanced Tin Supply

World tin production has been quite stable in recent years, with refined tin production between roughly 330,000 tpy and 370,000 tpy. This is made up from mine production between 270,000 tpy and 310,000 tpy, and the balance by 50,000 – 70,000 tpy of secondary refined tin production. Tin recycling will continue to play a significant role in future tin supply, however, whether the market share of secondary refined tin will grow or decline will depend on the balance between improvements in tin recycling technology and economics versus the falling concentrations of tin found in end-of-life products as a result of economisation. At a global level there is no reason to suggest that remaining tin deposits will be unable to sustain a long term, gradual upward trend in primary mined tin well into the future.

Resources and Reserves

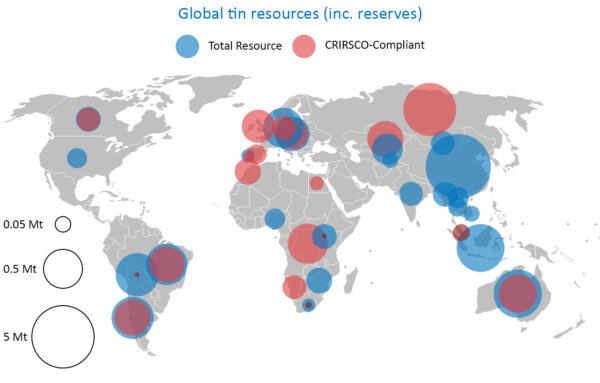

Resources and reserves refer to known deposits, which can be considered relatively few when compared to the vast potential for undiscovered mineral deposits. Even today, large areas of the earth’s surface have not been thoroughly explored due to lack of transport infrastructure, inhospitable terrain, weather conditions, wars etc., although the cost and difficulty of doing so means these areas are unlikely to lead to new deposits in the short or medium term. There is also significant undiscovered mineral potential at depth, particularly in regions like Africa where the majority of base metal exploration and discoveries have been at surface level over the last decade. Notably, reports on tin reserves do not account for likely future production from the important small scale mining sector where reserves are not considered at all. In contrast to many metals, a significant proportion of tin, typically 40%, is mined by local, individual, small scale or artisanal miners who do not carry out exploration or report reserves in the manner of large mine companies. For a full and comprehensive analysis of global tin reserves see the ITA Report on Global Tin Resources & Reserves.

Figures based on estimates available at the beginning of 2020

Tin Mining and Ore Concentration Techniques

- Underground mining: sinking vertical or inclined shafts with horizontal tunnels through hard rock to intersect the mineral veins at right angles where ore can be exposed.

- Dredging: mining alluvial deposits with large floating processing plants (dredges) on the surface of shallow seas or artificial ponds digging out tin-bearing sediments by means of an endless chain of buckets.

- Gravel pumping: washing tin-bearing sand from the face of surface mines to a lower pond with a high-powered jet of water, followed by collection from the base of the mine.

- Open cast mining: where ore is removed using mechanical shovels, excavators or manual labour instead of water jetting.

The main techniques employed for concentrating tin ores are screening, wet and dry gravity methods and magnetic and electrostatic separation. The amount of treatment needed depends on the grade of ore and type of deposit.

Tin Smelting and Refining

Once a tin concentrate of the required purity has been obtained (55 to 75% SnO2), it is sent to a smelter who smelts it into crude tin metal by removing the oxygen from the mineral. Many unwanted impurities are removed in the slag during this process, but additional remaining impurities are treated in the refining step (e.g. by heating under particular conditions in a cast iron kettle, or by electrolytic refining) where eventually, the refined tin of desired purity is cast into ingots for sale.

Standards of Operation

Leading members of the tin production industry, as members of the International Tin Association, are committed to reporting on the social, economic and environmental standards of their operations via the tin industry Code of Conduct. To learn more about the Code’s 10 principles and 70 standards please read more here Code of Conduct

Life Cycle Assessments (LCA)

Life Cycle Assessments (LCA) are a widely used technique to assess, understand and evaluate the magnitude and significant potential environmental impacts for a product system.

As part of its members’ commitment to sustainable development, The International Tin Association (ita) commissioned a LCA to quantify the environmental impacts of the production of refined tin. Full Member companies of the ITA, which were collectively responsible for approximately 55% of the global refined tin production provided data for the reference year 2018/2019. The study covered cradle-to-gate primary and secondary production and was undertaken according to ISO 14040 and ISO 14044 standards with a functional unit as 1 tonne of refined tin (99.95%).

The LCA included impacts associated with the extraction of resources from mining and beneficiation, and smelting and refining. The results are representative of the industry average for refined tin production, and therefore do not correspond with any specific technology route or region but are rather inclusive of the technologies being used by at least one of the producers participating in the study.

The outcomes generated from this LCA will inform stakeholders about the inputs and outputs and related environmental impacts for the production of refined tin and supplement LCA efforts undertaken by producer companies individually. ITA full member companies are committed to providing stakeholders with the most recent life cycle data and are working with ITA towards improving the accuracy of the data for industry average LCAs and demonstrating environmental improvements and efficiencies.

Download ITA Report ‘Life Cycle Assessment of Tin Production’

For further information or to discuss participation please contact [email protected]