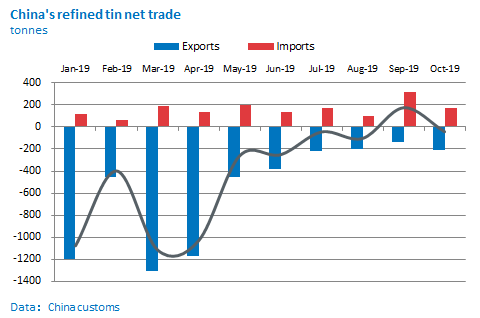

Despite the large arbitrage between the Chinese domestic tin price and the LME price, imports of refined tin into China were lower than expected in October.

China’s import arbitrage continued to widened from September as the SHFE tin price performed better than the LME. Usually, this is seen as an opportunity to import refined tin into the country. However, based on latest official customs statistics, China’s refined tin imports in October were just 170 tonnes, down 46% month-on-month (MoM), but up 25% year-on-year (YoY). In September, China’s refined tin imports were 314 tonnes, exceeding exports for the first time this year.

China’s import arbitrage continued to widened from September as the SHFE tin price performed better than the LME. Usually, this is seen as an opportunity to import refined tin into the country. However, based on latest official customs statistics, China’s refined tin imports in October were just 170 tonnes, down 46% month-on-month (MoM), but up 25% year-on-year (YoY). In September, China’s refined tin imports were 314 tonnes, exceeding exports for the first time this year.

Customs data also show that China imported over 12,500 tonnes of tin ore and concentrate in October, 12,000 tonnes of which originated from Myanmar. The estimated tin content of ore and concentrate imports in October was 3700 tonnes, down 35% MoM and up 12% YoY while that from Myanmar were 3400 tonnes, down 33% MoM and up 10% YoY. However, the estimated tin content of these imports so far this year were 41,100 tonnes, down 12% on the same period in 2018.

Our view: As a result of mine closures and lower imports, the Chinese concentrate market remains constrained. To relieve the pressure of the raw materials shortage, Gejiu Yunxin Non-ferrous Electrolytic Co., Ltd. announced that it will cease production for around 15 days for maintenance. However, this will only reduce refined tin production by some 200 tonnes over the short maintenance period.

Our view: As a result of mine closures and lower imports, the Chinese concentrate market remains constrained. To relieve the pressure of the raw materials shortage, Gejiu Yunxin Non-ferrous Electrolytic Co., Ltd. announced that it will cease production for around 15 days for maintenance. However, this will only reduce refined tin production by some 200 tonnes over the short maintenance period.

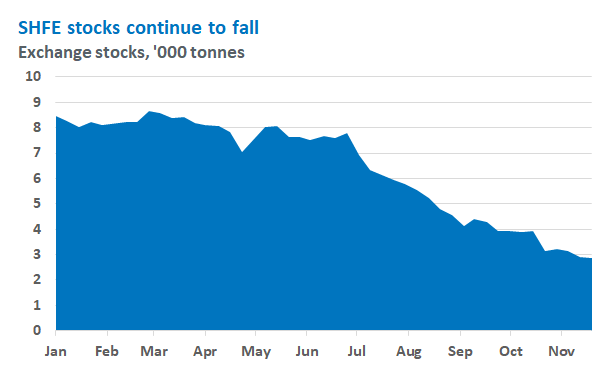

More noticeable is the decline in refined tin exports and falling SHFE tin stocks. While exports were high during the first half of the year on the back of the strong LME price and constrained Indonesian supply – up some 60% on H1 2018 – they have since fallen. Q3 exports of refined tin were down some 63% year-on-year. SHFE stocks have fallen from highs of 8,660 tonnes in March to just 2,966 tonnes on 29 November, a decline of 65%.

However, the tight market and fall in exchange stocks has not seen imports increase due to the lack of profit to be made on imported tin. Demand is reportedly satisfied by the current level of production, while imports are impacted by regulations. The most common grade of tin in China is 99.95% Sn, compared to a standard LME grade of 99.85% Sn, and so the spot market price for ex-China material can be up to some 3,000 yuan/tonne lower than the SHFE active contract futures price. Furthermore, material that is directly taken out of LME warehouses – where there is currently ample material – is even less profitable. Material on the exchange does not come with a certificate of origin, which importers of refined tin into China require to avoid significant additional tax rates.