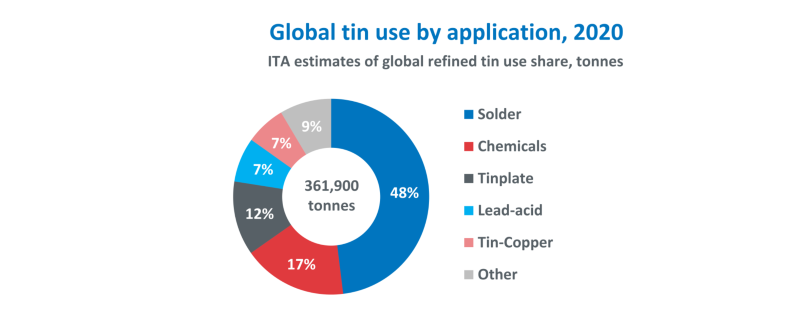

The seventeenth annual survey of tin users carried out by the International Tin Association (ITA) estimated that refined tin use in 2020 decreased -1.6% to 361,900 tonnes, with a preliminary estimate of 7.2% expansion during 2021, attributed to recovery from the COVID-19 pandemic. These data are much more positive than last year’s study, reflecting unexpected boosts to tin use such as working from home.

More recent data indicates that this could be overly optimistic based on use sectors being constrained by supply chain issues in H2.

101 companies took part in this year’s study, accounting for some 47% of estimated global refined tin use in 2020.

Refined tin stocks held by surveyed companies at the end of 2020 amounted to the equivalent of 2.6 weeks’ supply. If this ratio is extrapolated based on global consumption, it would imply that world consumer stock holdings were around 18,200 tonnes. Compared to data from 2019 and forecasts for 2021, consumer stocks grew in 2020. Forecasts for 2021 suggest that consumers are using up stocks they were able to rebuild last year.

Provisional estimates of total global tin use, including refined and unrefined forms, totalled 432,700 tonnes in 2020, down -1.7% from 2019. The Recycling Input Rate (RIR) was calculated to be 33.1% in 2020 and is forecast to fall slightly to 32.8% in 2021.

Solder still accounts for the largest global share of tin use, decreasing slightly to 48% in 2020. Forecasts for 2021 indicate global average increase of 8.8% related to rapid recovery from the COVID-19 pandemic, with RoW being much more positive at 15.9% YoY growth from -9.2% base in 2020. Electronics use sectors were boosted by increased working, education, and leisure from home. Respondents commented on future potential in 5G and related technologies.

The average proportion of lead-free solders in electronics grew to 80% globally in 2020, up from 77% in 2019. An increased 82% of specified tin use globally in lead-free solders was <100ppm Pb. The trend toward higher-purity, lower-lead specifications in tinplate also continued in 2020, as 79% of refined tin specified by reporting participants was <50ppm Pb, a marked shift from 45% in 2019.

In chemicals, tin use by survey participants was stable, reducing slightly by -0.6% in 2020 and forecast to grow by 1.6% in 2021. China markets were particularly impacted by the pandemic, balanced by much more positive feedback from the US where markets were boosted by residential construction related to an exodus away from cities.

Tinplate use reversed a long-term trend of being static or in decline, growing in the survey sample by 2.6% in 2020 and forecast by participants to continue increasing by 8.1% in 2021 due to increased canned food and beverage purchasing boosted by the COVID-19 pandemic.

Lead-acid battery tin use markets were relatively unaffected by the pandemic, growing by 2.3% in 2020 and forecast at 3.9% growth in 2021. Battery use was boosted for several reasons including increased replacement for idled car breakdowns. The major tin use effect in China was e-bikes which benefitted from those choosing not to use public transport.

Tin use in tin-copper markets largely maintained overall markets at -2.5%. Participants reported very optimistic forecasts of 20% growth in 2021 driven by new technology markets including electric vehicles and new electrical infrastructures. Other more traditional metal product markets were negatively impacted by around -15% in 2020, especially outside China, although forecast to rebalance to 1% growth in 2021. These sectors were hit hard by COVID-19 especially affected by automotive, engineering and giftware sectors. Increased float glass installations in China boosted 2020 tin use.