2021 saw refined tin production rebound from its pandemic lows, with the majority of global smelters – including many in the Top Ten – having a relatively “normal” year.

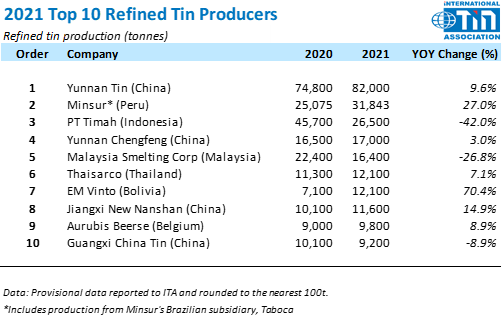

Yunnan Tin Company maintained its position as the world’s largest producer of refined tin, while others, such as EM Vinto, re-entered to Top 10 list. As was well-publicised at the time, MSC were subject to strict COVID regulations from the Malaysian government which saw its production fall significantly compared to 2020. Overall, global refined tin production is estimated to have reached 378,400 tonnes, up 11% on last year’s total of 339,400 tonnes.

ITA surveys global tin smelters to compile the annual list of the world’s largest producers. In 2021, these top 10 companies produced 59% of the world’s tin, down from 67% in 2020. As previously mentioned, the part of the drop in the group’s output can be attributed to the difficult year had by MSC. However, another significant decline in output from PT Timah – the second consecutive fall – also contributed.

In China, most smelters recovered production during 2021, despite challenges. Although recent imports from Myanmar has been lowered, some smelters have pivoted to importing concentrate from other regions – including central Africa. Producers in South America recovered rapidly from COVID-related issues in 2020, with all the surveyed smelters reporting increased production.

Our view: As expected, world tin production recovered well from COVID restrictions, exceeding 2019 and 2020 levels. We do not expect further COVID-related issues and foresee production to continue rising in 2022, with some 4% growth forecast.