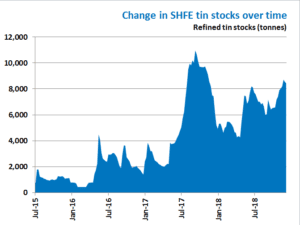

On 18th October, a standard warehouse warrant trading platform for tin, lead, zinc and nickel was launched by the Shanghai Futures Exchange (SHFE). Along with initial incentive schemes this has driven delivery of physical inventory into exchange warehouses.

SHFE has been incentivising use of the platform by waiving tin warrant trading transaction and transfer fees, although a storage charge of 1.5 yuan per day for one tonne of tin is being levied. In addition, a non-publicised incentive scheme currently rewards sellers 60 yuan per tonne of tin sold through the platform. This reward policy has driven more invisible delivery-brand tin stocks into exchange warehouses, increasing visible exchange stocks from 6,571 tonnes on 12th October to 8,425 tonnes as of 7th December.

More Chinese refined tin has been flowing from smelters to traders because of an arbitrage between the futures and spot market since the launch of SHFE tin futures on 27th March 2015. Now, Chinese smelters seldom hold refined tin stocks, except state-owned companies and Yunnan Chengfeng. Many traders use the tin warrant as a financing instrument, and the tin warrant trading platform makes the operation more flexible.

Our view: We believe that high SHFE tin stocks reflect the newly incentivised delivery of invisible stocks into exchange warehouses. In reality we expect that total Chinese physical tin stocks are in decline because of recent and ongoing smelter production issues. Our preliminary forecast indicates China will destock 9,700 tonnes of refined tin this year, taking production, consumption and net trade into account. This destocking is mainly due to a sharp decline in Q4 refined production and relatively strong exports this year, especially in the first half.